Misinformation Mondays: What Social Media Has Wrong

The “Everything Is Gambling” Fallacy

We haven’t done a Misinformation Mondays post in a while, but something so egregious landed on our desk that it demanded a response.

The first Misinformation Mondays Award of 2026 goes to…

Jeff Edelstein.

He recently wrote an opinion piece titled Everything is Gambling and We’d be Better Off Admitting It.

There are so many issues with his article that we couldn’t possibly litigate them all here, but his core thesis, as you can surmise from the title, is this:

Every decision you make in which you can’t know the outcome is, on some level, a bet. You’re putting something on the line, be it money, time, emotional energy, your digestive system, what have you, and hoping it works out. You might have information. You might have skill. You might have a gut feeling. But you don’t have certainty. And the absence of certainty is what makes it a gamble.

And there it is: The grand confusion, again–Conflating uncertainty and gambling.

The proliferation of this reasoning is precisely why it feels like everything is gambling nowadays. When people spread the notion that those ideas should be collapsed, everything becomes a gamble. Buying a house? A gamble. Eating lunch? A gamble. Crossing the street? A gamble. By definition, the future is uncertain because it is difficult to predict. So if uncertainty equates to gambling, then from one point to the next, your entire life would be a gamble.

But that is not analysis–its wordplay.

The practical world doesn’t work that way. People must make decisions under uncertainty. Families buy homes. Investors buy stocks. Collectors collect. Walkers cross the street. Traders trade. Economic activity requires forward-looking decisions, and because of that, societies had to develop actual gambling laws to distinguish between legitimate economic activity and gambling.

And that brings us to the real problem.

Gambling Is a Legal Term–Not a Vibe

Edelstein’s misinformation is twofold:

Conflating uncertainty and gambling; and

Using “gambling” as a moral judgment.

This confusion is older than the country itself. Alexander Hamilton struggled with it, trying to distinguish “honest Men” from “unprincipled Gamblers.” The ambiguity only grew from there, and the consequences worsened. So much so that our inaugural LexBeyond podcast was dedicated to this very topic.

So what is gambling then? The truth sits somewhere between “everything is gambling” (Edelstein’s position) and “nothing is gambling” (an unserious statement).

The topic is complex, but the basics can be delivered in three pictures. Internalize these and you’re in the top 1% of the curve.

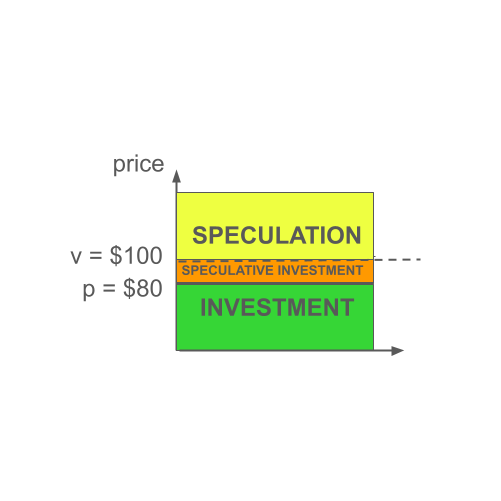

The Stock Market is Never Gambling

Regardless of how it feels, no matter how many losing trades are made, it isn’t gambling. For every Warren Buffett disciple who actually takes time to value businesses, there are a hundred others simply buying stocks with zero understanding of cash flows. A lack of serious analysis and valuation. Just vibes.

Is that reckless? Yes.

Is it gambling? No.

There’s already a word for reckless trading: Speculation.

Think of this like Al Pacino’s line in Scent of a Woman: “But not a snitch.” He wasn’t endorsing everything Charlie did, he was identifying the one thing that mattered the most.

Same concept here. The stock market isn’t the Church, and traders aren’t nuns and priests. But put potential fraud aside, and at the end of the day, there are only two things you can do in the stock market:

Investing; or

Speculation.

The transition zone between them? That is known as speculative investing:

The concept is not complicated:

Price below value + margin of safety → Investing

Price below value but shrinking margin → Speculative investing

Price above value → Speculation

Buying blind with no valuation → Speculation

Two quick reminders:

There’s no such thing as “value investing.” That’s a myth. (podcast)

Crypto (including Bitcoin)? Never investing, pure speculation.

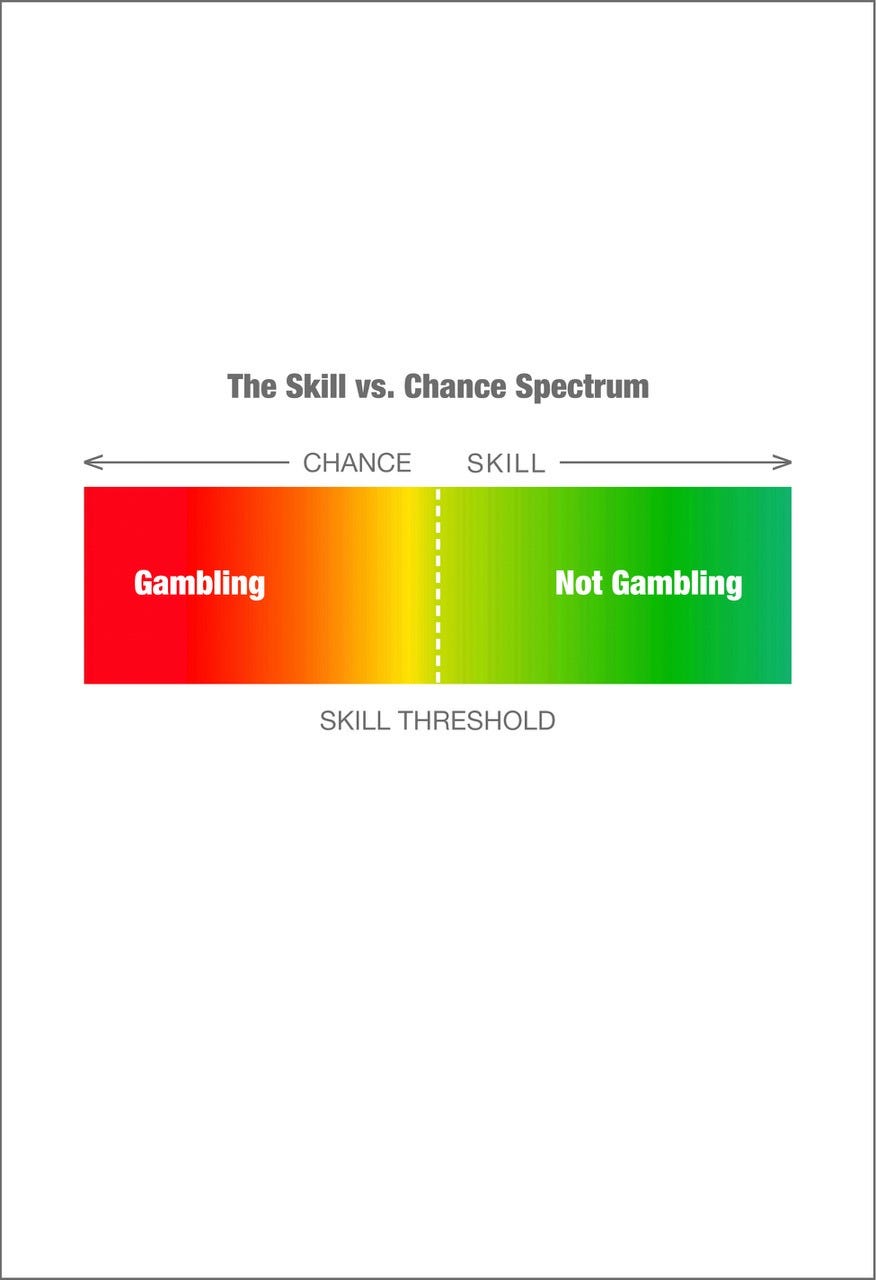

Games - The Skill vs. Chance Spectrum

Assuming the prize and consideration legs are satisfied–you pay something of value and receive something of value–how do we know whether a game is gambling?

Simple: Skill vs. chance.

Chess is pure skill.

Roulette is pure chance.

Poker sits near the middle.

The difficulty is not in the framework–it’s the measurement. It would be difficult for society to agree on, say, poker is 55% skill and 45% chance because one can’t even agree on whether the Earth is round. And on the off-chance that there was consensus on it, some states would classify it as a game of skill and others as a game of chance because the skill threshold you see above is set differently by each state.

But don’t confuse measurement difficulty with framework ambiguity. Variations of the framework have been in place since England began legislating gambling in the 14th century. America inherited the English common law foundation, including statutes like the Statute of Anne. From there, it continued to evolve and the level of skill is undisputedly the threshold question now.

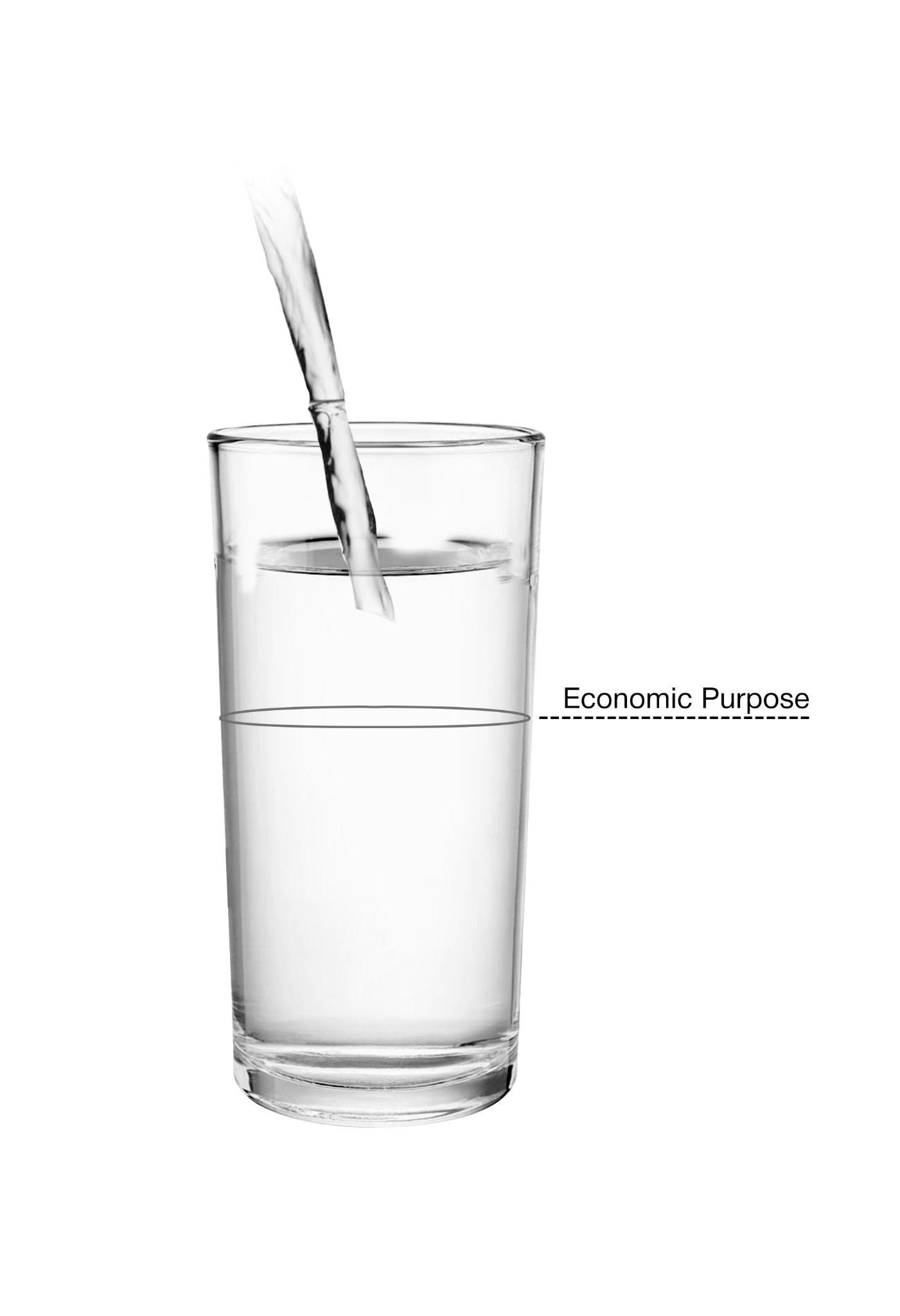

Futures–The Hard One

This is the most complex category, but the image helps internalize it.

Futures also sit on a spectrum. In fact, you could redraw the game spectrum from above and simply replace “skill” with “economic purpose, ” and “chance” with “entertainment.” Same idea, different visuals.

So why is this one harder?

Because the real fight isn’t how to determine when a futures product becomes gambling–it’s whether we’re supposed to determine that in the first place. We’ll detail this in tomorrow’s post over on our sister blog, Full Court Press. In fact, it’s so important that we will be exploring the topic in detail in our upcoming book: Predictable.

But allow us to give you a quick history:

Pre-1974: The informal test was hedging utility. Futures existed for risk management.

1974: Congress codified the economic purpose test. Products needed economic purpose to be approved.

2000: Congress inexplicably repealed the test and dismantled the approval process. Exchanges could self-certify.

CFTC’s response: Ignored the repeal and continued using the economic purpose test as their North Star.

2010: Congress added the word “gaming” to the statute (but not “gambling”), left it undefined, and cleaned up parts of the mess.

CFTC’s response: Doubled down (with even more law and legislative history on their side), utilizing economic purpose as their guiding principle.

2024: The CFTC shattered the glass. As Selig made clear on Odd Lots, the agency no longer sees itself as a merit regulator.

So, are prediction markets gambling?

Through the economic purpose lens: Most of them, yes.

Through Kalshi’s own lens: also yes.

But here’s the tension:

“Gambling” appears nowhere in the Commodity Exchange Act.

For 175 years, America tried to keep gambling separate from futures trading (the CFTC’s view also, not just ours).

Congress never defined gambling (with respect to futures trading)–even after the biggest economic crisis in modern history.

The CFTC is clinging to that ambiguity like it’s the last lifeboat on the Titanic (they became the promoter and are no longer a bona fide regulator).

And the smoking gun?

The statute does contain the word “gaming.”

If gaming = gambling (our view of what Congress meant), the economic purpose glass still holds.

If gaming includes sports games (Kalshi’s earlier view), the CFTC is still a merit regulator–at least for sports gambling.

If neither? Then for the first time in 175 years, the boundary between futures and gambling disappears and may never return.

You decide, America.

The stakes are real. The definitions matter. And the confusion Edelstein promotes–collapsing uncertainty into gambling–is exactly how we lose the ability to regulate anything with coherence.