A Survey of “Value Investors”

Part II - Seth Klarman

First and foremost, our heartfelt condolences go out to the family, friends, and admirers of Charlie Munger. His profound influence and wisdom have left an indelible mark on the financial world. In honor of his legacy, we plan to pay a fitting tribute with a proper eulogy before the arrival of the New Year. Charlie Munger, you will be deeply missed, but your contributions will continue to inspire generations to come.

In our previous post, we started out on a journey exploring the realm of the so-called “value investors.” You might wonder why we are putting the phrase in quotation marks. We do so, because we think the phrase is a dangerous myth. Are we splitting hairs? While the term may sound like semantics, it serves as the gateway to an entirely transformative paradigm. Contrary to nitpicking, this misnomer acts as a linchpin that unlocks a door to the original and correct understanding of investing.

In this paradigm, Bitcoin finds no place in the esteemed Three Stock Lunch segment of CNBC’s Power Lunch, nor does it belong to a balanced investment portfolio, as argued by a recent Bloomberg columnist. In this universe, it becomes less clear whether the net effect of endless crypto trading is a positive one for society. We don’t think Bitcoin will be shut down as suggested by Jamie Dimon, but it certainly shouldn’t share the same sentence with investing. In this alternative world, those drawn to Bitcoin for speculative gains, dreaming of a luxurious Lambo, may still engage. Similarly, individuals seeking utility from Bitcoin, whatever form that may take, could also participate. However, true investors maintain a cautious distance, recognizing the absence of cash flows, rendering Bitcoin’s intrinsic value at zero and categorically excluding it from the realm of genuine investments.

In this paradigm, “value investing” may actually make a comeback, despite David Einhorn’s skepticism, who, notably, was the first “value investor” profiled in our series. A revival of this magnitude would necessitate Einhorn and his counterparts to candidly acknowledge their prior missteps and rebrand their operations as the only way to invest.

How big will the appetite for investing be in this altered landscape? That remains uncertain, but it is unlikely to wane from the current levels. Those who align with the value philosophy will persist as buyers, joined by perhaps a fresh cohort of investors embracing this recalibrated approach. There exists a segment of the population uninterested in speculation; both individuals and institutions within this group may redirect their focus, and wallets, from cryptocurrencies to cash-flow-generating assets once they recognize that, all along, they haven’t been investing.

Market conditions could play a pivotal role in accelerating such a reversal. The younger generation hasn’t seen a true recession. Older market participants have lived to tell about it, but the human tendency is to forget. The enduring desire to preserve capital always resurfaces, and when it does, the demand for genuine investing will likely ascend, concurrently diminishing the allure of speculation.

In this transformed landscape, the prospect of Bitcoin being characterized as a security seems increasingly plausible. Why wouldn’t it? If the primary motive behind its widespread acquisition is ostensibly for investment purposes, despite the fallacious nature of such a premise, the question arises: Shouldn’t those who identify as “investors” be entitled to protective measures?

This common-sense conclusion, underscored in our recent amicus brief, faces obfuscation due to what we perceive as a misguided application of the Howey test. While delving into the intricacies of this topic is more apt for our sister blog, The Full Court Press, we’ll leave you with this succinct point: There exists a straight line connecting the misconception of “value investing” to the fate of a trillion-dollar economy. The ramifications of this misconception warrant careful consideration in navigating the evolving intersection of cryptocurrencies and securities regulation.

Far from splitting hairs, we see the acknowledgment that all investing is value investing as a monumental paradigm shift in the world of finance. The longer this misconception persists, the more entrenched it becomes, amplifying the magnitude of this transformative shift.

Why, then, have we strayed so far from this financial truth? One reason, we posit, is the group of people who haven’t made the effort to understand the essence of investing and have instead accepted what the market has promoted to them. We believe the bigger reason, ironically, involves brilliant minds, individuals who dedicate considerable time to thinking things through and articulating insightful perspectives, yet somehow do not conclude that “value investing” is fundamentally a misnomer. Enter Seth Klarman:

Seth Klarman a veritable legend in the financial world, serves as the CEO and portfolio manager of The Baupost Group, a prominent Boston-based investment manager with over $27 billion of assets under management (AUM). Klarman wrote a book called Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor. It is out of print and has acquired a certain rarity, so you may have to pay thousands of dollars to get your hands on it.

In a podcast appearance, he explains why he chose that title for the book (around 1 hour 23 minutes mark):

I still love that I stole the title blatantly from [The] Intelligent Investor, because it is such a great expression, and it really captures what a value investor tries to do. You need to leave room, because you might be wrong, markets might go against you, but if you are patient, you can find a margin of safety and having one means you are likely not [going] to be in tears when a lot of other investors are. (emphasis added)

Seth Klarman’s description of the concept of the margin of safety is absolutely correct. However, where he goes off course is in defining this practice as exclusive to value investors. This is the very thing that every investor does anyway!

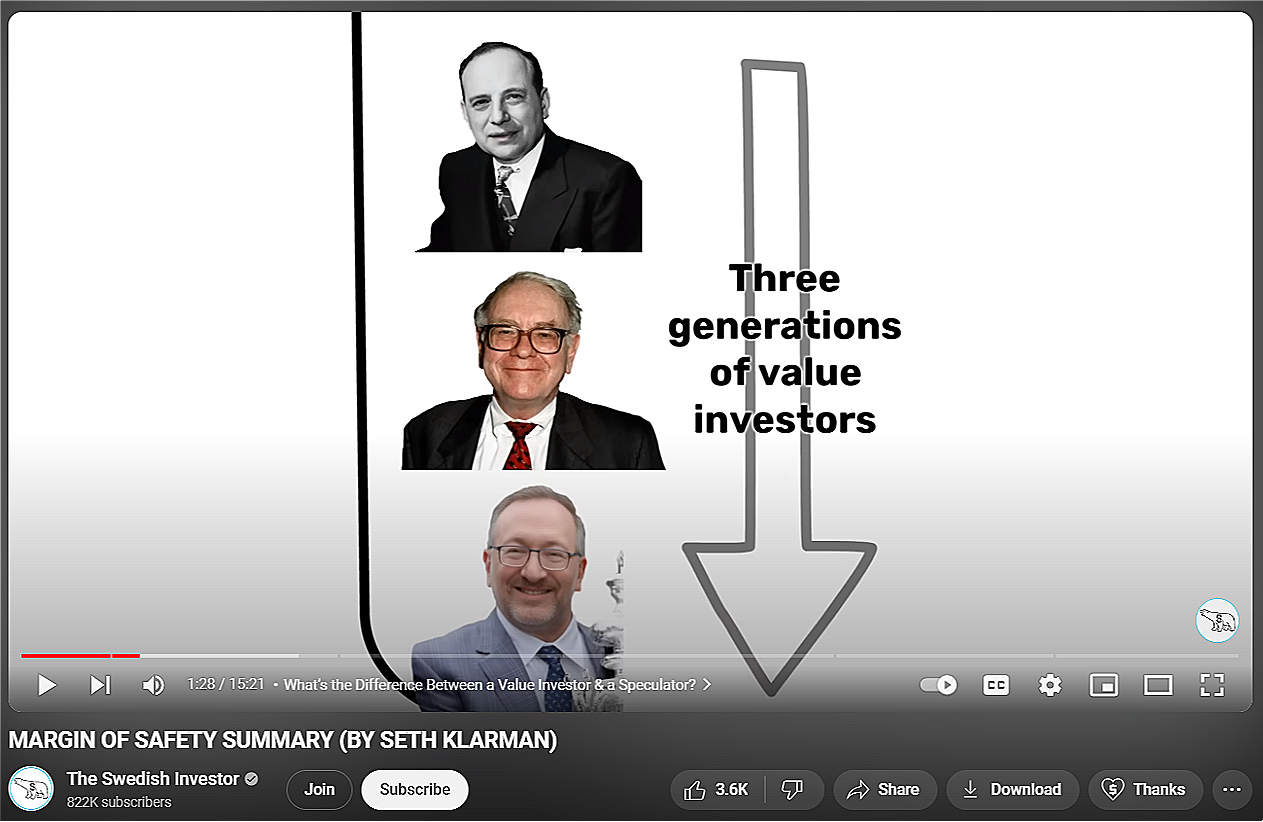

Seth Klarman is viewed by many as the heir apparent to the Ben Graham/Warren Buffett/Charlie Munger lineage. The New York Times aptly described him as “the most successful and influential investor you have probably never heard of.” This snapshot from a YouTube video on Margin of Safety is a perception that many people hold:

100 years from now, AI-generated images will likely fill the annals of financial history, competing for the best visual award that describes where we have gotten off track. No need to wait that long, we may already have a winner above. If financial historians are looking for a turning point, this is precisely where you find it.

Why? The power of the visual above is twofold: First, it misidentifies Graham and Buffett as value investors. Second, by creating a straight line from Graham and Buffett to Klarman when there is none, it provides intellectual protection to Klarman and his cohort of “value investors.”

While it might percolate for years, the truth is this: Seth Klarman, or anyone else identifying as a value investor, stands apart from the traditional lineage of Graham, Buffett and Munger. This assertion is not a slight against Klarman at all; his brilliance, evident success and articulate communication are beyond question. At the same time, the very concept of “value investing” clearly deviates from the principles taught by Graham, Buffett and Munger.

The key difference between Graham/Buffett/Munger and the class represented by Klarman is that the former group does not perceive themselves as value investors. This may strike you as nonsense, especially considering the notion that Ben Graham is the “Father of Value Investing,” and Buffett and Munger are considered the greatest value investors of the last half-century. Indeed, there is an abundance of resources –books, articles, videos– that further enhance these perceptions. Here is just a small sample of links:

Benjamin Graham and “Value Investing”

Investopedia

Motley Fool

UCLA Benjamin Graham Value Investing Program

Columbia Business School The Heilbrunn Center for Graham & Dodd Investing

Warren Buffett and “Value Investing”

Investopedia

Buy Side from Wall Street Journal

Barron’s

Investing.com

Charlie Munger and “Value Investing”

Are they all wrong? “They” being all these sources that describe Ben Graham, Warren Buffett and Charlie Munger as “value investors”?

What truly differentiates us is our willingness to delve into the depths of understanding, far beneath the surface level. Recognizing that myths can survive for extended periods, we acknowledge that a widespread belief doesn’t necessarily equate to truth. Popular opinions, while influential, don’t necessarily validate the accuracy of a concept. Our commitment to this level of scrutiny allows us to navigate the layers of financial philosophy and challenge these prevailing narratives when necessary.

The relevant query, of course, is what Graham, Buffett and Munger themselves said about value investing. While you might think that’s an obvious approach, our observations reveal a notable lack of scrutiny on the original sources.

Filtered through the joint lens of history and logic, the results are unequivocal and markedly different from the prevailing narrative. Ben Graham, Warren Buffett and Charlie Munger do not perceive themselves as value investors. Instead, they perceive themselves simply as investors. This nuance not only challenges conventional wisdom and underscores the importance of revisiting primary sources to uncover the authentic perspectives of these financial titans, but it also is a distinction that entirely reshapes the world of finance, not to mention the issues that are being heavily litigated.

Starting with Ben Graham, his nickname is the “Father of Value Investing.” If you buy his masterpiece, The Intelligent Investor, today, it will ship with the subtitle The Definitive Book on Value Investing. Then, there are of course many “value investing” references circulating ubiquitously, which we sampled above, including educational programs at top institutions like Columbia and UCLA that are named after him. If your first reaction is that we are delusional, we can’t blame you. There is certainly something to be said about realizing that what you have believed all your life may have just been a giant misunderstanding.

That said, please bear with us here for a minute. It would be hard to imagine a scenario where a father doesn’t talk about his child, wouldn’t it? Similarly, it should raise eyebrows that Ben Graham, often dubbed the "Father of Value Investing," never once used the phrase "value investing" in his two seminal works, The Intelligent Investor and Security Analysis. Does it make sense to you that the “Father of Value Investing" would never utter the phrase in either of his two bestselling books that have shaped financial thought for decades? He is the wrong father.

A bit shaken by the discovery? You might be wondering: Why would a book contain “Value Investing" in its subtitle if it is never mentioned anywhere in the book? Also, what about Warren Buffett? Surely, he must have used the phrase hundreds of times. The answers to these questions are connected.

We know Buffett has used the phrase value investing three times in The Superinvestors of Graham-and-Doddsville, an article that was published in the Fall 1984 issue of Hermes, a Columbia Business School magazine. It later made it into the 1986 edition of The Intelligent Investor as an appendix. We have always believed that to be the reason why the phrase “value investing” may have made it into the book’s subtitle in the first place; it was a made-to-order phrase for a book publisher that may have been looking for a more catchy subtitle. In case you are wondering, the phrase “value investor” is nowhere to be found in any of the editions of The Intelligent Investor that were published before Ben Graham died in 1976, namely the 1949, 1954, 1959, 1965 and 1973 editions.

Does that automatically make Buffett a believer? Luckily, we also have the benefit of Buffett writing his infamous investor letters every year, so we have a live track record, a window into what he was thinking at any given time. Surely, if Buffett were a true believer in “value investing,” he would have written about it all the time, wouldn’t he? If you were to scour his letters though, you would only see the phrase twice. The first one came in his 1988 letter. Then, he mentioned it once again in his 1992 letter. Most importantly, though, in that second and last mention, Buffett made a very important clarification:

In addition, we think the very term "value investing" is redundant. What is "investing" if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value - in the hope that it can soon be sold for a still-higher price - should be labeled speculation (which is neither illegal, immoral nor - in our view - financially fattening). (emphasis added)

With that last mention, Warren Buffett set the record straight a long time ago, but the myth of “value investing” lives on.

Were we able to plant some seeds of doubt in your mind? We hope so because all evidence points to this whole “value investing” myth as having created a lot of confusion. If you are so inclined to look into Charlie Munger’s body of work to find a supporter, we’re afraid you won’t be able to find it there either. To be clear, you can find footage of him using the phrase “value investing,” when he was asked about the future of value investing. Analyze his statements holistically, however, and it becomes clear that he aligns with Graham and Buffett. Among other things, Charlie Munger denounced “value investing” as a bad use of the language. He said:

I think it’s a bad use of the language to think there is a difference between value investing and other good investing. All good investing is value investing, by definition. (emphasis added)

The world describes Ben Graham, Warren Buffett and Charlie Munger as “value investors.” We suppose doing so gives them intellectual armor, and an opportunity to leverage from the celebrated legacies of Graham, Buffett and Munger. The problem? The “celebrated” don’t share that view at all.

What exactly makes the word “value” in “value investing” redundant? Where is the logical issue in using it as a qualifier before the word investment? Expanding on these inquiries, let’s start with how Seth Klarman describes the state of the world, in particular, the two types of market participants: value investors and speculators.

Here is another snapshot from the video we referenced above, the one that summarizes five takeaways from Klarman’s Margin of Safety.

What is “value investing" according to Klarman? He offers his definition in the podcast we referenced above, around the 18-minute mark:

TED SEIDES: When you went to launch Baupost, you were in still the early years what was called and probably still is value investing. I’d love to hear how you define value investing.

SETH KLARMAN: The key definition for value investing comes from Graham and Dodd, and the idea of it is, that because markets are inefficient, prices deviate from value. And, that deviation, sometimes they fall below underlying value, and that makes them a value investment, it makes them attractive. Other times they get to full value and maybe even significantly exceed it, at which point you should have sold, and if you were inclined to be a short seller, perhaps shorted it.

And what does he view as speculation? That we can find in the 7th Edition of Security Analysis, a Graham and Dodd masterpiece, which Klarman edited.

In recent years, some have attempted to expand the definition of an investment to include any asset that has recently appreciated in price--or might soon: art, rare stamps and coins, wine collections, NFTs (nonfungible tokens), and hundreds of alternative (crypto) currencies. Because these items generate no present or future cash flows and have values that depend entirely on the buyer whim, they should be regarded as speculations, not investments.

He is 100% correct. What Klarman doesn’t realize is that he and others clinging to the concept of “value investing" is, in large part, what made this possible.

You might ask, how? It is because of how humans rationally process information. If your child comes home from the first day of basketball practice and tells you that there were some short kids on the team, what is the first inference you would make? There must be some tall kids on the team. If that wasn’t the case, and everybody was about the same height, that’s not how your child would have described it when they came home.

Along the same lines, if the market participants are constantly hearing that there is this niche investing philosophy called “value investing,” they rationally conclude that there must be some other ways to invest. Otherwise, the word value would be redundant. And it absolutely is redundant, something Warren Buffett realized more than 30 years ago. It is a bit of a mystery why all the intelligent people who consider themselves disciples and students of Warren Buffett ignored that point entirely.

In The Well-Meaning Sultan and Geometry: A Tale, we told a hypothetical story about how calling squares equal-sided-squares confused the kids even more. Recognizing that the concept of “value investing” is ultimately a logical fallacy, we also offered a logic-focused explanation relying heavily on Venn diagrams. In both cases, our goal was to drive the point home that adding an unnecessary qualifier leads the mind, quite rationally, to concluding the activity is just a subset of a broader set, and once that conclusion is made, to look for things that fill the gap. That is the biggest irony of all: Whether it was out of misplaced allegiance to Graham and Buffett, or, value investors re-branding investing as “value investing” perhaps looking for a differentiator in the marketplace, “value investors” diminished their own value proposition, and created fake competitors. Simply put, speculation rose because investing was reduced to value investing.

The question we’d love to ask Seth Klarman is this:

What other types of investing are out there besides value investing?

There must be something, right? The word value qualifies investing, implying that is just a subset. What, then, fills the space between value investing and investing?

We know he will not say art, or crypto, or NFTs. He’d be right. What else is left then? Growth?

Remember, Buffett summarily rejected the growth vs. value distinction (and he is right). Others, such as Howard Marks, co-founder and co-chairman of Oaktree Capital Management, also seem to be coming around on it (we’ll profile Marks later in this series). Most importantly, though, Seth Klarman himself is not a buyer of the growth stock vs. value stock narrative:

For those who are not in a position to click on the video, this is what he said:

The academic definition of value is buy the stock that is cheapest by the numbers. But I don’t think that’s what Graham and Dodd wanted, in fact it's clear that they were talking about earnings power and the growth possibilities in a business even if they are hard to determine. So I think value has to be determined for every company. The way I think about the market is not that there are growth stocks and value stocks, but rather that all stocks may hold value. (emphasis added)

Once again, Klarman is 100% correct here. Where things go wrong is Klarman not taking this argument to its natural conclusion. If growth investing is value investing in disguise, which it is, and crypto, NFT, etc. purchases are speculation, which they are, there can logically be only one conclusion. The word “value” is redundant, as Buffett said in his 1992 letter, and all investing is value investing, which is what Charlie Munger concluded.

Seth Klarman, on the other hand, uses the phrase extensively. In the preface to the 7th Edition of Security Analysis alone, he used “value investing” or “value investors” more than 60 times! Yes, we counted; to put things into perspective, he used it more than once per page, on average.

The unfortunate thing is that Klarman’s preface is great otherwise. Other than a couple of disagreements with him that pale in comparison to his usage of “value investing,” the preface is full of amazing insights. It is something that every market participant should read, in fact, it should be required reading for any financial literacy class. It is clear that Klarman took the time the piece deserved, and thought about every word.

Except for “value investing,” it seems like. Why Klarman, clearly a person of high intellect is critically thinking through everything, but not through the very phrase that is fundamental to everything is a big puzzle for us. What is it that prevents him from reaching the same conclusion that he should have no problem reaching, one that was reached by both Buffett and Munger? The unfortunate result is that a piece of great insight will also likely end up being a powerful myth perpetrator, and might take its place in the history books as yet another milestone that reinforces the misconception of “value investing.”

Even worse, the 7th edition is the first time in history that the phrase “value investing” made its way into the subtitle of Security Analysis. As they say, history repeats itself.