Why Charles Schwab Is One Step Away from Dominating Financial Services

One small step for Schwab, one giant leap for Schwab

Schwab is setting itself apart…

Nuance is rare in financial markets these days, which is why Schwab’s recent comments on prediction markets were so refreshing. In the Q1 2026 earnings call, CEO Rick Wurster drew a line that almost no one else in the industry has been willing to draw: A line between financially relevant event contracts that serve the public interest and pure entertainment gambling.

That distinction matters more than people realize.

When analyst Devin Ryan (Citizens JMP Securities, LLC) asked about prediction markets, Wurster didn’t hedge:

Devin, I think you hit the nail on the head in terms of how we think about it, which is we do differentiate between financial-related events and sports, politics, pop culture. At Schwab, we believe in the power of ownership and the power of compounding over time and owning equities, owning fixed income assets, being an investor over time and having that ownership leads to higher levels of wealth. And our goal as a company is to help our clients live their best financial lives. And so prediction markets that are not aligned to that are not something that we want to pursue.

Decrypt summarized it perfectly:

Rick Wurster sees a big distinction between speculation on Taylor Swift’s love life and the latest inflation numbers.

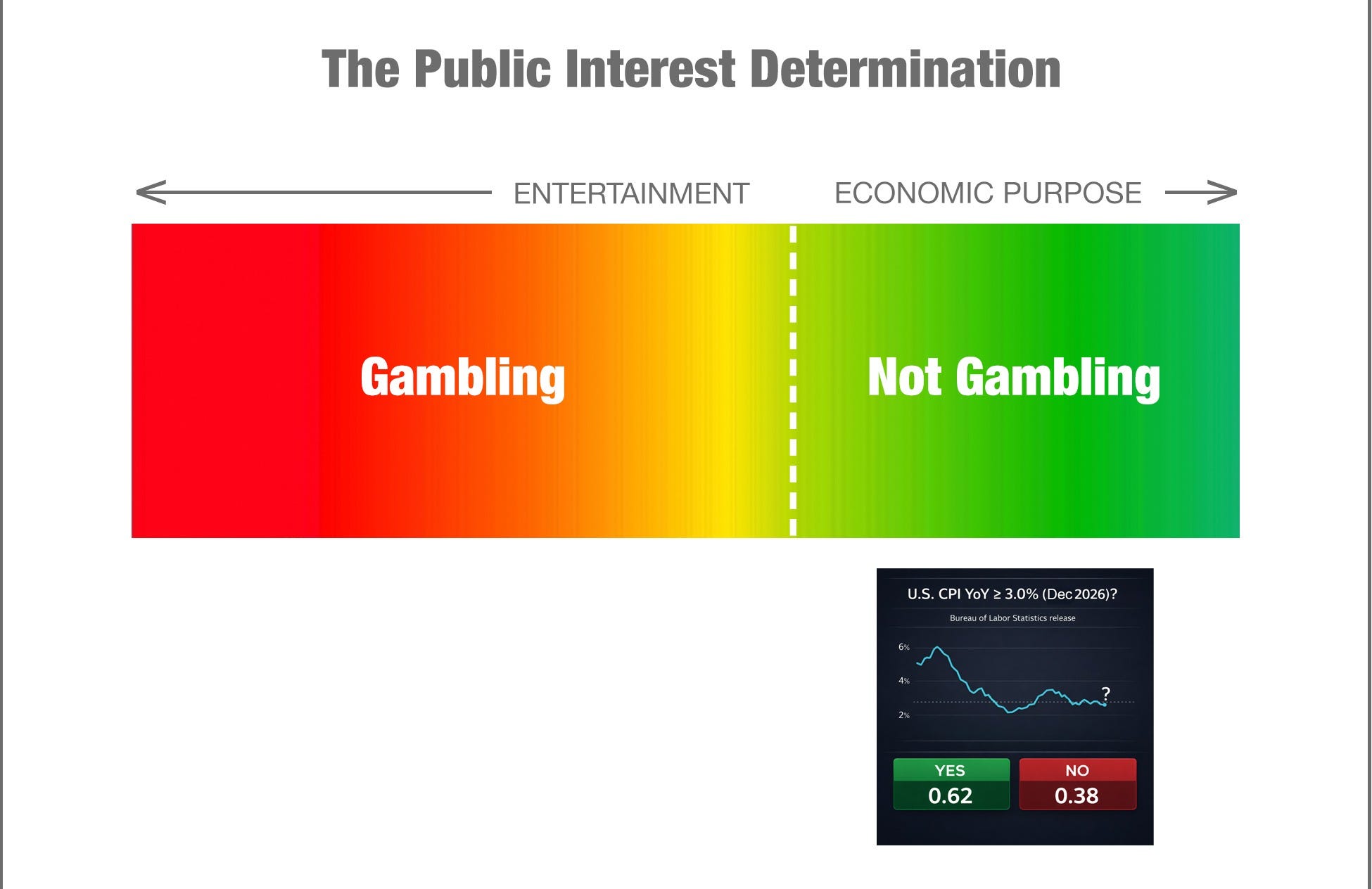

Paul Grewal doesn’t necessarily see it that way, but we do. The determination of whether something should be allowed or not depends on where it falls on a spectrum. The correct regulatory answer has never been “ban everything” or “allow everything.” The answer is–and always has been–somewhere in between those two elements.

For event markets in particular, we created an image for you: The top panel visualizes how event contracts are supposed to be evaluated. The next step is the placement of any event contract along this spectrum so a regulatory decision can be made. Below, we did this for inflation contracts:

The idea is simple.

If a contract benefits society, it’s not gambling.

If it’s pure entertainment, it is.

All event contracts are located somewhere on this spectrum. The inflation contracts can legitimately be used for risk management, so we place them (so does Wurster) on the socially beneficial side of the spectrum.

Wurster continued:

And if you look at the stats on the success of gamblers, they’re not strong and people generally lose money. And so as a company that is in business to help people live the best financial lives, we have kept sports and other things off to the side.

“People generally lose money.”

That’s a correct statement as evidenced in Dune’s “Polymarket Trader Cashflow PnL:

To be clear, that a large percentage of people losing money is not what makes it gambling. A company managing its exposure to inflation via event contracts may very well lose money also, the same way many people “lose money” on their car insurance. Successful management of a material risk is what they get in return, and that’s beneficial.

More broadly though, Wurster’s stance around separating socially beneficial contracts from entertainment vehicles is not only correct, it’s strategically brilliant.

The Option Schwab Is Quietly Buying

Inflation contracts are not the sexiest. Sports and parlays still dominate prediction-market volume. Crypto markets picked up some, but as of April 18, 2026, 90% of the volume (on Kalshi) was still sports + parlays. Remove sports and the industry craters. Remove sports and elections? The industry then becomes nothing more than a niche.

But if you extract the useful contracts–inflation, oil prices, certain corporate events–and embed them inside a Schwab-scale ecosystem, the calculus changes and they stop being toys and start being tools. An investor long Exxon might want a hedge tied directly to oil prices. Today they are using options. Tomorrow, they might prefer a binary event contract.

It’s not going to be Schwab’s best-selling product, but it doesn’t have to be. It will be a product that will maintain the company’s long-standing tradition of helping customers live their best financial lives.

Is this enough for Gen-Z? Wurster seems to believe Schwab is already winning the Gen-Z race, so perhaps it is. Wurster is effectively buying an option for Schwab–giving him a reputation card to hold in his back pocket. His nuanced view on prediction markets is arguably akin to an out-of-the-money option right now.

And if SCOTUS eventually cracks down on the entertainment side of prediction markets? Wurster will get to say, arguably, the four most valuable words in finance:

“We told you so.”

If the regulatory environment shifts, the option becomes deeply in-the-money overnight, Schwab becomes the responsible adult in the room and today’s out-of-the-money option comes to fruition.

If that’s the direction Wurster is headed, he is be planting the seeds for dominating the financial services sector for the next two generations.

And if he refines his messaging on this decade’s other financial darling, crypto, he will be optioning yet another category for substantial future gains.

Crypto: The Other Option Schwab Should Be Buying

Schwab’s new spot-crypto trading platform is another opportunity, but also another messaging risk. The press release starts strong with this quote from Jonathan Craig, Head of Retail Investing at Charles Schwab:

We know our clients want to conduct more of their financial lives at Schwab. With Schwab Crypto, clients who want direct access to the asset class can trade it alongside their other investments, while benefiting from the service, education, and research they expect from us.

So far, so good. Notice the careful wording. It doesn’t say one can invest in crypto. It uses the word “trade.” It’s intentional and it’s disciplined.

But as the press release elongates, the messaging begins to drift into confusion:

“A holistic crypto investing experience”;

“Digital asset investments”; and

“Incorporat[ing] digital assets into their portfolios.”

Does Schwab view crypto as just another form of investing? That appears to be the case. In fact, customers that sign up for the e-mail newsletter are greeted with a similar message before they even click on it:

Explore crypto investment opportunities and resources…

And if they actually scroll through that e-mail and make it to the bottom of the disclaimer, their goodbye finally appears:

Due to the high level of risk, investors should view digital currencies as a purely speculative instrument.

What excites a customer is the first thing they see. The thing they should really know is in the fine print.

A good friend and I were discussing this exact same issue over Christmas break. He challenged me on my thesis and my proposed policy idea around labeling. His critique captured it perfectly: “Don’t companies already say what you want them to say–just in the disclaimers?”

That was a very astute observation, which is also the exact issue at hand. My response to him, which will also double as my reply to similar future feedback is:

Put it in the fine print, you protect yourself.

Put it in the headlines, you protect investors.

The way Schwab communicates its crypto trading platform to its customers is the best market example that drives that point home. If they were to simply flip that order, leading with clarity instead of burying it, they’ll win the next 50 years.

The Real Definition of Investing (and Why it Matters)

We have written extensively on why Bitcoin is not investing, so we will not rehash it here. Bottom line: Investing requires cash flows. No cash flows, no investing. That principle, which was uncontroversial a century ago, is now long forgotten. Buffett hanging up his cleats certainly does not help:

Schwab’s own educational content tries to separate investing from gambling, but it stumbles on one phrase (hidden in a post Craig published back in October 2025):

Investing, on the other hand, is the allocation of capital to a business or asset with the expectation that it will generate income or appreciate in value.

Not every purchase is an investment; the price has to be right, too. But the more perilous expansion to investing comes from the last three words: “appreciate in value.” Craig’s post was well-intentioned, but those last three words encapsulate where the entire modern confusion begins and certainly where I disagree.

The starting point of the confusion seems to be the fact that:

i) Stocks can be investments (at the right price); and

ii) You can make money on stocks in two ways (not necessarily exclusive): Dividends and price appreciation.

Here comes the inference that seems natural to many, but what is, at its core, simply a logical fallacy:

Since investable assets can appreciate in value, an appreciation in the value of any asset implies that the asset was an investable asset.

It’s true that a stock can appreciate in value, without giving you a cent in income. You can buy low, sell high, and voila–you made money. But remember, it’s the process that counts, not the outcome–that’s the core of investing:

If appreciation alone makes something an investment, then what about the following conclusions1:

Gold is an investment;

Crypto is an investment;

NFTs are an investment;

Baseball cards are an investment; and

Beanie Babies are an investment.

I’m nearly certain that if I were to ask Craig whether he thinks Beanie Babies are an investment, he’d say no. Schwab, after all, has already discredited that idea:

The friends’ enthusiasm for the toys is contagious, and soon the demand for these cute stuffed animals, called Beanie Babies, is growing so quickly that people are treating them as investments.

Exactly. Notice the tone here, which is absolutely crucial: It’s not Beanie Babies are investments; but people are treating them as if they are. Treating something as an investment doesn’t make it one.

My stance on this is clear. The only coherent boundary for investing is the one finance has been using for a century:

Investing requires cash flows.

Speculation does not.

To be clear, I am not saying people shouldn’t buy those things, and by extension, it doesn’t mean Schwab can’t offer them. I simply mean that the boundaries should be clearly drawn. Limiting people’s choices is not the answer, arming them with clarity is:

Could Schwab decide to choose this path and bring its views about crypto speculation to the forefront rather than burying them in a disclaimer? Sure they could, and if they do, this could be a transformative move that separates them from the competition for the next two generations.

The Better Path: The One Schwab Is Already Halfway Down

Schwab’s own press release ends with a mission statement that contains the answer:

At Charles Schwab, we believe in the power of investing to help individuals create a better tomorrow. We have a history of challenging the status quo in our industry, innovating in ways that benefit investors and the advisors and employers who serve them, and championing our clients’ goals with passion and integrity.

I also believe in the power of investing. But to harness that power, we must first properly define it. I find it very difficult to adopt a definition that leads children to believe that they can invest in Beanie Babies.

If Schwab truly wants to challenge the status quo, they should complete this 3-step playbook:

Step 1: Equities trading → Investing

(if price < value)Step 2: Crypto trading → Speculation

(offer it, but label it honestly)Step 3: Prediction markets → Risk Management

(offer the essential subset only; label the rest as gambling and do not offer it)

Schwab is already doing Step 1 and Step 3. In actuality, they are also doing Step 2, but they’ve buried it so deep within their disclaimer language it’s hardly transparent. If Schwab were to take that additional step and flipflop the fine print to the headlines, they will become the industry leader around transparency:

Put it in the headlines, you protect investors.

Put it in the fine print, you protect yourself.

The con: Schwab may lose a few customers, sure.

The pro: Schwab becomes the alpha. They become the out-of-the-money option that can be exercised in the future for pure domination.

That type of transparency is what separates the wheat from the chaff. The long-term reputational benefit may very well outweigh the loss of a few customers.

Consider this: I’ve already speculated that we will be facing a financial crisis in the near future and that 2029 may be the year:

If we face that systemic crisis, with prediction markets and crypto leading the way, Schwab will have already taken the first step by distancing itself from event contracts that don’t serve the public interest (because they are non-essential: frivolous or recreational):

If they take just one more step and label crypto as speculative? Not in a disclaimer, but in the headlines? If they can do that, Wurster and his executive team, and Schwab as a whole, become the authoritative firm that saw it coming, labeled it correctly and protected their clients.

That is how you dominate financial services for two generations.

Bottom Line: Transparency is the Alpha Move

I have always believed that the SEC should become a label regulator. We once hoped that the SEC would get there by 2027, but under the current administration, that is very unlikely to happen. It is also unclear whether it will happen with the next one. We started this blog with an aim to spark change, to achieve industry consensus that would eventually trickle into regulator action by 2027 (hence our blog name and logo).

It’s already April 2026, and perhaps that goal was too ambitious. So maybe the solution isn’t regulator-led, but corporate-led. And no company is better positioned right now than Schwab.

They already have the scale.

They already have the trust.

They already have a nuanced worldview.

They simply need the commitment to put the truth in the headline instead of the fine print.

One small step for Schwab.

One giant leap for Schwab.

The implicit assumption here is that the assets do not produce cash flows.